Table of Content

Where the home secures a mortgage, the homeowner's insurance company is required to issue any checks for the claim (often called "loss drafts") in the name of both the homeowner and the lender. As a result, homeowners will need to contact their lender to obtain their endorsement on any claim checks or start the claims process, which is dependent on loss amount. If you have an escrow account on your loan, we will typically pay property taxes out of your escrow account for the home that secures your loan. Making payments biweekly allows you to make 13 regular monthly payments, or one extra payment each year that is applied to your principal balance. Along with the discounted interest rates on variable home loans, customers can save $600 on establishment fees and a minimum of $96 on ongoing loan maintenance fees. Assistance in getting offset accounts, redraw capabilities, and extra repayment plans.

This is because, banks want to stop people re-borrowing more than they can reasonably pay back within the original loan term. Following the backlash, they’ve decided to change back home loan redraw limits for any customers who wants it. Any excess funds that you’ve put in your home loan is essentially earning you the same rate charged on your home loan.

Partial Offset Account

Where there is a second or subsequent mortgage to another financial institution. Home Loan Experts is a business owned by mortgage broking firm Home Loan Experts Pty Ltd. We can help you navigate the often complex pre-approval and application process.

Mortgage Insurance protects your lender in case you default on your loan. Mortgage insurance is generally included in your monthly mortgage payment. For more information about your homeowner's insurance requirements, select the link New American Funding Guide to Hazard and Flood Insurance.

Comparing NAB home loans

New American Funding is listed on the check because we are the loss payee on the insurance policy. We are required to be the loss payee on the insurance policy by the loan owner which has a secured interest in the property. Our responsibility is to ensure the property is repaired in the event of damage and restored to its original or higher value. Lender-placed insurance is insurance coverage that we obtain if we do not have proof that you have adequate insurance coverage in place to protect our interest in your property. Because the coverage goes into force without an inspection of your home, the policy is often more expensive than an insurance policy that you could obtain yourself. Further, lender-place policies may provide less coverage than an insurance policy that you could obtain yourself.

In order for your homeowner's insurance to meet the investor and insurer requirements that apply to your loan, it must cover damage from wind. However, in some states, wind damage is allowed to be excluded from homeowner's insurance policies. If your homeowner's insurance excludes wind coverage, you will need to obtain a separate Wind Insurance policy. Your payment will be withdrawn from your bank account on the date specfied. Borrowers can benefit from discounted premiums on selected insurance products and lower interest rates.

How Do I Apply?

Keyboard_arrow_down Home Loan Types Should you get a professional package, fixed rate loan, basic home loan, 100% offset loan, equity loan, line of credit or low doc loan? 100% Offset Account 100% offset accounts allow you to use your everyday funds to reduce the balance of your loan. This can drastically reduce your interest, saving you thousands! Basic Home Loan Are you after a basic home loan with the cheapest interest rates and no ongoing fees?

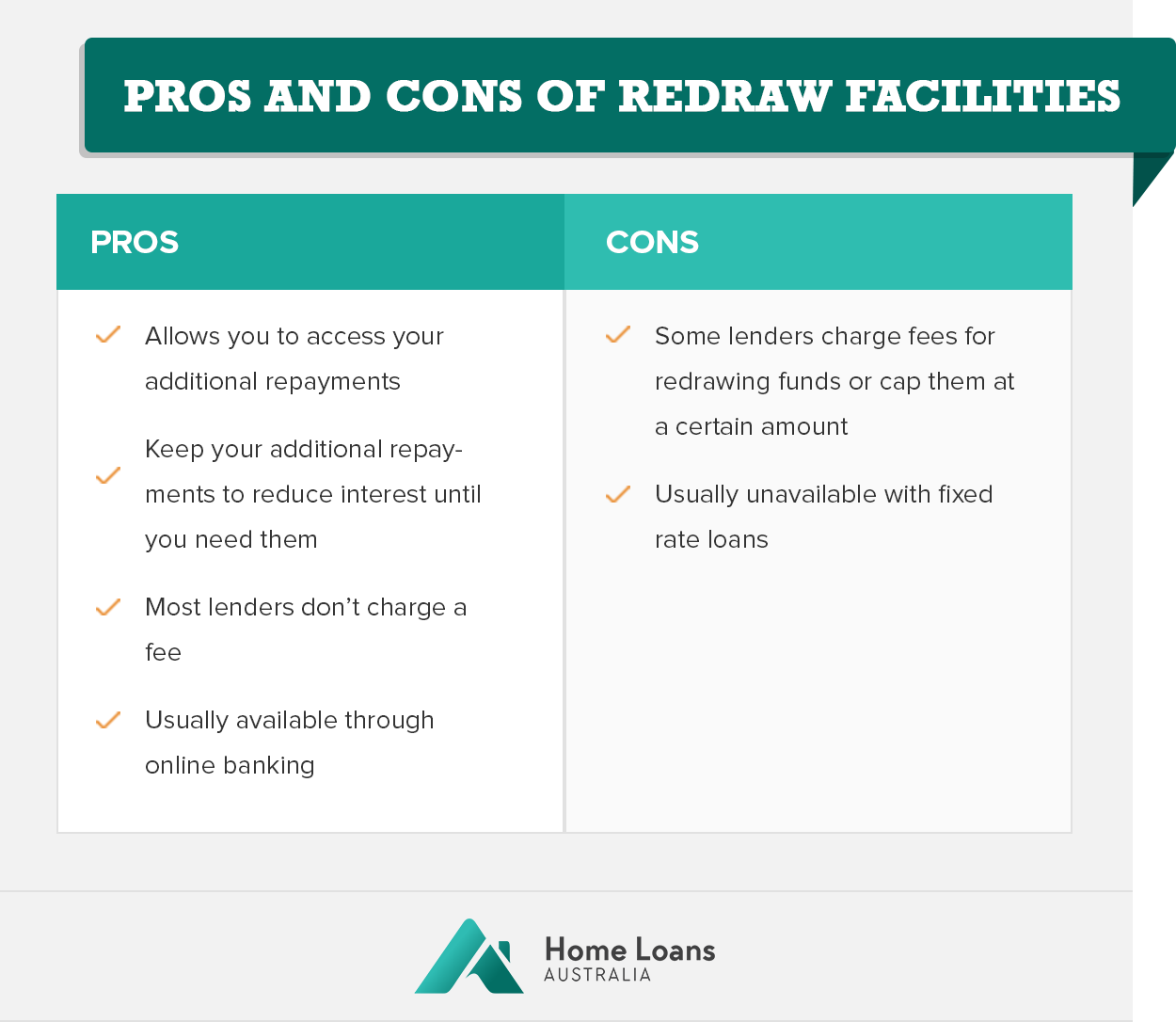

This means you’ll have money available to take back out – if you want to. One of the benefits of making extra repayments on your home loan is being able to redraw some of those funds. So you can make the most of this feature, we explain how it works and how it can help you achieve small or large goals. The offerings are subject to errors, omissions, changes, including price, or withdrawal without notice. Loans are a big expense for most people and it can be costly to switch lenders.

What's the difference between a redraw facility and an offset account?

However, you may not redraw an amount if it would result in the balance owing on your loan account exceeding the amount which would be owing if you had paid all scheduled repayments on time. For loans insured by the Federal Housing Administration , mortgage insurance is required on all loans, regardless of the down payment amount. You cannot file a claim against the policy, and generally cannot cancel it. More information on FHA Mortgage Insurance can be found in our guide download below. Whether you are looking to switch from another lender or want more affordable rates on your NAB home loan, they can help.

It is important to note that each state has its own rules, regulations, and requirements for its specific program. Delinquent VA and FHA loans do not qualify for Stamp & Go, regardless of the total claim amount. You can find the total claim amount for your insurance claim on the Loss or Damage Report or Adjuster’s Worksheet that you should receive from your insurance adjuster. Free features are available for customers like offset accounts and redraw facilities. Vehicle and equipment loans are subject to credit assessment and approval. Home Loan Experts has mortgage brokers with years of expertise working with NAB.

In most cases, you will save no money by making your monthly mortgage payment early. Your fixed rate mortgage payment has been calculated to determine equal monthly payments to pay off the loan by the end of a defined term, typically 30, 20 or 15 years. The amount of interest due each month is based on the mortgage monthly interest rate and the outstanding loan balance on the last day of the prior month. Since mortgage payments are made in arrears, unlike rent payments, there is no benefit by paying early. You can calculate the interest to be paid on your next monthly mortgage payment by multiplying the monthly interest rate times the outstanding mortgage balance at month-end.

The cost to switch your home loan can vary depending on what you want. For example, if it’s a better interest rate, you need to make sure the savings from the lower rate are enough to justify the cost of refinancing, which includes exit fees, application fees and other charges. Luckily, our refinance calculator and borrowing power calculator are great ways to estimate these expenses so you don’t get surprised later.

If you’re switching your loan, you should consider if the new loan type has a redraw facility. For instance, if you switch from a Standard Variable Rate to a Fixed Rate home loan you will no longer have access to a redraw facility during the fixed-rate period. We are required to analyze your escrow account at least one time a year. If the analysis shows an overage in your escrow account, it is because we collected more than we needed over the past year to pay your escrow bills. When this happens, we are required to send the excess funds back to you in the form of a refund check.

No comments:

Post a Comment